Executive Summary

Premium trust accounts often appear healthy because balances reconcile and controls pass at month-end. Yet beneath that surface, timing mismatches, reversals, suspense, and misallocations can quietly create material liquidity risk.

Trust-compliant does not always mean “cash-flow safe,”. This article outlines where hidden trust risk accumulates within MGA operations and what a controlled, real-time operating model looks like to ensure remittance integrity, liquidity clarity, and sustained carrier confidence.

Introduction

Trust failures rarely begin with a mistake. They begin when reconciled balances create false confidence, masking timing gaps and allocation risks that only surface under scrutiny.

Premium trust accounts are designed to protect carriers and insureds by keeping premium funds separate from an MGA’s operating cash. On paper, that separation feels safe: the trust account balance is visible, bank statements reconcile, and the ledger ties out at month-end.

But “trust-compliant” doesn’t automatically mean “cash-flow safe.”

Premium trust is one of the easiest places for an MGA to accumulate hidden liquidity risk not because anyone is doing something wrong, but because timing, reversals, and allocations rarely line up neatly across policy admin, billing, payments, and accounting. The risk often stays invisible until reconciliation, a carrier inquiry, or an audit forces the full story into view.

Here we break down where that risk hides, why it’s common, and what a stronger trust operating model looks like without assuming any specific system.

Why can the Trust Account Look Healthy While you’re Actually Exposed

The core issue is simple:

A bank balance is not the same thing as “available trust cash.”

When teams treat the trust account like a single pool of funds, rather than a controlled subledger with restrictions, cash-flow risk quietly builds.

For carriers, this distinction matters because remittance delays or shortfalls are rarely caused by a single failure, but by accumulated assumptions about availability. For MGAs, the danger is operational confidence built on totals instead of restricted cash reality.

Five Common Sources of Hidden Cash-Flow Risk

Across audits, carrier reviews, and operational deep dives, the same patterns surface repeatedly. These are not edge cases; they are systemic behaviors driven by growth, scale, and operational fragmentation.

- Timing mismatch: booked premium vs cleared cash vs remittance due dates

Most MGAs operate with multiple “clocks”:

- Policy clock: premium is bound/invoiced/recorded

- Payments clock: cash clears days later (or reverses later)

- Carrier clock: remittance is due on specific cycles

- Producer clock: commissions are calculated and paid on another cycle

If your process collapses these into one concept—“premium received”—you can accidentally remit or pay out against cash that hasn’t truly settled or is not truly available.

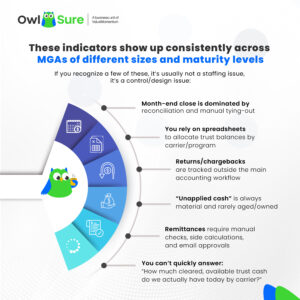

How it shows up: the trust balance is fine on paper, but you’re scrambling when remittances are due because actual cleared cash isn’t where you thought it was. -

Chargebacks and ACH returns that unwind allocations after the fact

Card chargebacks and ACH returns create a unique trust liquidity risk: they arrive after money was applied and distributed.

A common chain:- premium is received and applied to a policy

- amounts are allocated to carrier/fees/commission

- remittance planning assumes funds are stable

- then a chargeback/return hits and pulls cash back out

- now the trust account is “short” unless allocations unwind correctly

If reversals are handled manually or outside the core workflow, this becomes one of the fastest paths to trust imbalance.

How it shows up: recurring “mystery shortages,” increasing suspense, frequent manual adjustments, or delayed remittances. -

Mixed funds across carriers/programs/entities without a true subledger

Many MGAs run multiple programs and carriers but maintain a limited number of trust bank accounts. That can work—only if there is a rigorous internal structure that tracks restrictions at the transaction level.Without that, teams end up doing allocations in spreadsheets (or ad-hoc rules) to answer basic questions like:

- How much is owed to Carrier A vs Carrier B?

- What portion is premium tax/fees?

- Which funds belong to which entity/program?

A spreadsheet can reconcile totals while masking that a specific carrier/program is underfunded.

How it shows up: carrier disputes, remittance corrections, and “it reconciles overall, but not by carrier.” -

Suspense and unapplied cash becoming a permanent parking lot

Suspense is normal. Permanent suspense is a warning sign.

Unapplied cash grows for predictable reasons—missing policy numbers, mismatched invoices, partial payments, duplicates, lockbox ambiguity, producer-side delays. The risk isn’t that suspense exists; it’s that it becomes operationally “acceptable” and stops being governed.

When unapplied cash sits too long, the MGA loses the ability to confidently state what portion of trust is truly available versus “unassigned.”

How it shows up: increasing write-offs, late reallocations, manual cleanup during close, and poor forecasting of remittance capacity. -

Bordereaux and late adjustments that create retroactive truth

Bordereaux often functions as the moment reality catches up: late endorsements, cancellations, reinstatements, mid-term adjustments, premium corrections, and backdated changes.

If you don’t have strong traceability from:

policy transaction → cash receipt → allocation → remittance → adjustments,

then bordereaux becomes a recurring surprise that forces backtracking across multiple months.How it shows up: fire drills each bordereaux cycle, retroactive corrections, and tension between underwriting/ops/accounting on “what’s correct.”

Practical Warning Signs Your Trust Model is Carrying Hidden Liquidity Risk

What “Good” Looks like: Trust as a Controlled Operating Model, not a Monthly Reconstruction

High-performing MGAs treat trust operations as continuous financial infrastructure, driven by financial systems and GL modernization, not as a periodic accounting cleanup.

The goal is not just to reconcile, it’s to operate trust continuously with controls that make the truth visible in real time.

A stronger trust model typically includes:

Clear definitions (that everyone uses)

- Cleared vs pending cash

- Restricted vs available trust cash

- Suspense categories + aging + ownership

- Standard treatment for returns/chargebacks

- Policy-level traceability for allocations and adjustments

Transaction-level allocation (not just totals)

Every receipt should be traceable to:

- policy / customer

- carrier/program

- premium vs tax vs fees

- commission/producers payable

- status (pending/cleared/reversed)

Exception-driven operations

Instead of hunting issues during close:

- exceptions are queued daily/weekly

- suspense is aged and owned

- mismatches are resolved upstream

- reversals automatically trigger review and unwind logic

Remittance confidence

You should be able to produce, on demand:

- what’s due to each carrier (and why)

- what cash is actually cleared and available

- what adjustments are expected

- what is being held in suspense and for how long

By automating financial operational flows and exception handling, OwlSure helps MGAs and carriers replace manual reconciliation with continuous trust controls. Teams gain on-demand visibility into carrier obligations, suspense aging, reversals, and remittance readiness, improving accuracy, audit confidence, and operational scale.

Closing Thoughts

Trust failures are rarely sudden. They are slow-building control gaps that compound quietly.

Premium trust accounts don’t usually fail because of one big mistake. They fail because small timing and allocation gaps compound until a remittance cycle, reversal wave, or audit exposes a shortage that was always building quietly.